Market research · 2025 · 5 min read

UK Confectionery Market Analysis

Defining a 'healthier indulgence' positioning for a £8.4bn category, built from PESTEL, Porter's Five Forces, and a segmentation that landed on 18-34-year-old office workers as the realistic primary target.

- Context

- University of Sheffield · MSc Strategic Marketing & Branding

- Role

- Team project (4) -- research and segmentation lead

- Duration

- 10 weeks

Frameworks applied

- PESTEL

- Porter's Five Forces

- Segmentation, Targeting, Positioning

- 4Ps marketing mix

The brief

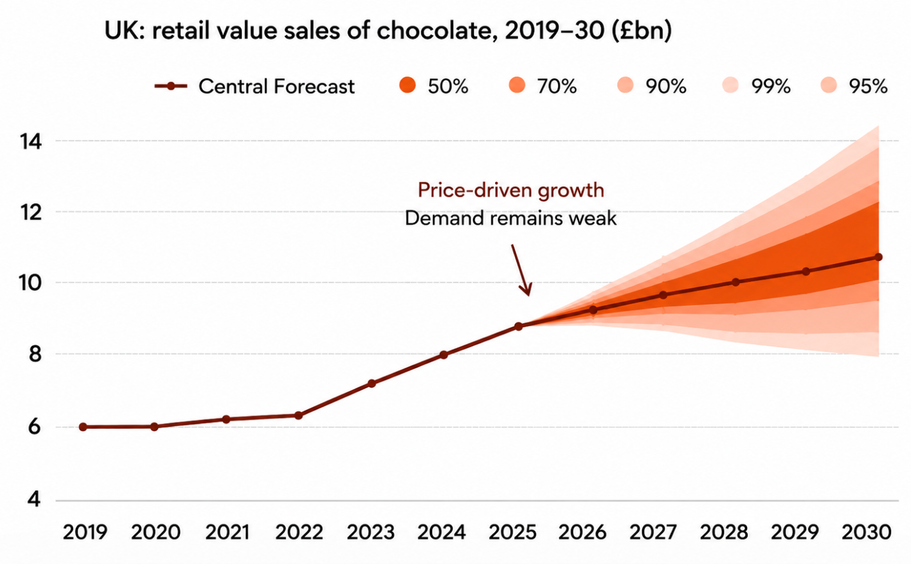

The UK chocolate confectionery market is worth £8.44bn in 2025, up 10% year on year -- but that growth is driven by price increases, not volume demand. Forecasts point to £10.3bn by 2030, yet the underlying trend is a consumer base buying less frequently and spending more carefully. Health-led entrants are eroding the assumption that taste and indulgence are the only attributes that matter. The team was asked to recommend a positioning and full marketing mix for a hypothetical new entrant -- but the strategic question was the harder one: who is the realistic first customer for a confectionery brand launching today?

UK chocolate retail value sales 2019--2030, central forecast with confidence intervals. The market is growing in value -- but driven by price, not volume. Source: Mintel.

Method

We worked the analysis from the outside in: macro forces, then competitive pressure, then customer.

PESTEL mapped the macro shifts. The two that mattered weren't the obvious ones (sugar tax, regulatory scrutiny) but the slower structural shifts: the post-pandemic premiumisation of small everyday treats, and the durable rise of "permission" snacking -- products positioned as deserved-rather-than-allowed.

Porter's Five Forces showed the category's economics with painful clarity. Buyer power is high (supermarket retailers control shelf), supplier power is low (commodity ingredients), and the threat of substitutes is structurally rising (savoury snacks, premium chocolate, "better-for-you" categories). What this meant for a new entrant is that the only durable defence is a differentiated brand position, because none of the operational levers are available.

Segmentation, Targeting, Positioning. Using Mintel, Statista, and Innova data, we segmented the UK confectionery buyer along three axes -- life-stage, occasion, and motivation -- and identified three viable consumer segments:

- Impulse buyers (18--34) -- convenience-driven, self-purchase, emotional reward on the go. Our primary target.

- Family sharers -- motivation centred on sharing and value, bulk and family-format purchase.

- Health-conscious consumers -- wellness and quality focus, premium and dark chocolate.

We chose the smallest of the three.

The three segments mapped by motivation, behaviour, and competitive risk. We chose the impulse buyer -- the smallest of the three.

Why impulse buyers, and not the bigger segments

The two larger segments -- families, and health-conscious premium buyers -- are commercially attractive but already well-served by incumbents with massive distribution and shopper-marketing budgets. A new entrant cannot win on shelf next to Cadbury Dairy Milk in the family segment, and cannot compete with Lindt on premium credibility, on a launch budget.

The 18--34 impulse segment is smaller but structurally different. Its primary purchase occasion is the workday -- afternoon energy dip, Friday celebration, post-meeting reward -- which is largely won at convenience-format retail and online subscription, not the supermarket main aisle. That changes which competitors a new brand has to beat, and changes which channels matter.

"Healthier indulgence" -- what we mean by it

Positioning was the part of the project that required the most discipline, because "healthier indulgence" is a phrase a hundred brands have already used badly. The framing we settled on was:

A treat that takes the guilt out without taking the indulgence out.

This is a deliberately narrow claim. It rules out two adjacent positions that look similar -- "healthy snacks" (too clinical, kills the indulgence) and "better-for-you chocolate" (too generic, already crowded). The wedge is the office worker who wants a 3pm reward she can have without the residual self-criticism that follows a Twix.

The 4Ps

Product. A small range, intentionally limited. Three SKUs at launch with measured sugar content, recognisable ingredients, and a portion size designed for a single workday occasion -- not the big sharing format that dominates the supermarket aisle.

Price. Premium to mainstream confectionery (so the "permission" framing reads as earned), but explicitly below the "luxury chocolate" price band (so it reads as everyday-affordable rather than special-occasion).

Place. Convenience-led: high-footfall office-adjacent retail (Pret, Boots, WHSmith), Deliveroo / Uber Eats partnerships for afternoon office orders, and a thin online subscription tier for the loyal segment. The supermarket main aisle is explicitly not a launch priority.

Promotion. A content-led, social-first launch focused on the workday occasion specifically -- afternoon dip, Friday-feeling, the small reward. Not "healthy" as the headline message; "earned" as the headline message.

Strategic recommendation

Targeting the impulse buyer through three mutually reinforcing moves:

| Focus | Insight | Strategy | Expected impact |

|---|---|---|---|

| Digital-first reach | Consumers are buying less frequently in a value-conscious market | TikTok and Instagram content, influencer partnerships focused on the afternoon occasion | Increase impulse conversion |

| Affordable formats | Value-driven behaviour is rising; shoppers are not abandoning indulgence, they're managing it more carefully | Small-pack SKUs at a price point that fits a tighter budget | Maintain purchase frequency |

| Better-for-you positioning | Consumers still seek affordable, convenient indulgence -- but increasingly want to feel good about it | Functional and wellness chocolate innovation positioned around the "earned treat" | Strengthen brand preference and premium perception |

The logic connecting all three: a brand that meets consumers where they are financially (small packs, accessible price), earns their attention where they spend time (TikTok, Instagram), and gives them a reason to feel good about the purchase (better-for-you credentials) has a path to frequency and loyalty that neither the family segment nor the premium segment offers a new entrant at launch scale.

What I would test first

The whole strategy depends on one assumption I would put real budget against before scaling: that the office-worker afternoon occasion is large enough, and exclusive enough to convenience-format channels, to support a meaningful launch on its own. A two-city pilot -- one with full convenience-channel distribution and one without -- would resolve that question in three months and tell us whether the segmentation is right or whether we need to widen the target before going national.